If you bought your home in 2021 or 2022 when rates were at historic lows, you may be sitting on significant equity. If you locked into a higher fixed rate in 2023 or 2024, the current rate environment may now justify breaking that mortgage early. Either way, May 2026 is shaping up to be one of the most compelling windows for Canadian homeowners to reassess their mortgage—and that represents a major opportunity for mortgage brokers.

This guide breaks down everything your clients need to know about refinancing in Canada right now: what it costs, when it makes sense, and how to calculate whether the numbers actually work.

What Is a Mortgage Refinance, Really?

A refinance means replacing your current mortgage with a new one. It is not a renewal — renewal happens at the end of your term and does not change the amount you owe. A refinance is a fresh mortgage application, often with a new lender, a new rate, and potentially a new loan amount.

The most common reasons Canadians refinance:

- Access Home Equity (Equity Takeout): Tap into the equity built up in your home as a lump sum—for renovations, debt consolidation, investing in another property, or education. Lenders typically allow borrowing up to 80% of appraised value.

- Secure a Lower Interest Rate: If rates have dropped meaningfully since signing, long-term savings can outweigh the cost of breaking the term and paying a penalty. Even a 0.50% reduction on a $500,000 mortgage saves ~$2,500/year in interest.

- Consolidate High-Interest Debt: Mortgages carry far lower rates than credit cards or personal loans. Rolling high-interest debt into a refinanced mortgage dramatically reduces monthly outgoings and simplifies finances.

- Extend the Amortization Period: Extending from 15 to 25 years lowers monthly payments and improves cash flow. This requires a full refinance—it cannot be done at renewal without re-qualification.

- Switch From Variable to Fixed (or Vice Versa): With rate uncertainty persisting, some homeowners want payment predictability. Others want to capitalize on the lower variable rate now that the Bank of Canada has paused.

When Can You Refinance—and When Should You?

There is no mandatory waiting period in Canada. Technically, you could refinance the day after closing on your new home. But whether that makes financial sense is a very different question.

- Best: At Renewal

No prepayment penalty applies. Most homeowners refinance here — usually 5 years in. Zero penalty removes the biggest single cost. - 120 Days Before Renewal

Many lenders allow the refinance process to begin up to 4 months early, penalty-free. Lock in today’s rate without waiting. - Mid-Term: Run the Numbers First

Breaking a closed fixed mortgage mid-term triggers an IRD penalty. Always calculate the break-even point before proceeding. - First 1–2 Years: Rarely Worthwhile

IRD penalties are highest early in a fixed term. Legal fees add $1,000–$3,000 more. Combined costs almost always outweigh savings.

Broker Tip

Clients on a variable or adjustable mortgage face a penalty of only 3 months’ interest — typically $1,000 to $3,000. This makes mid-term switches to a fixed rate far more viable than breaking a fixed mortgage. With the Bank of Canada paused, this conversation is highly relevant right now.

What Does It Cost to Refinance in Canada? (2026)

Refinancing costs typically fall between $1,000 and $3,000 in fees — before the prepayment penalty, which is usually the largest single cost. Here is a full breakdown:

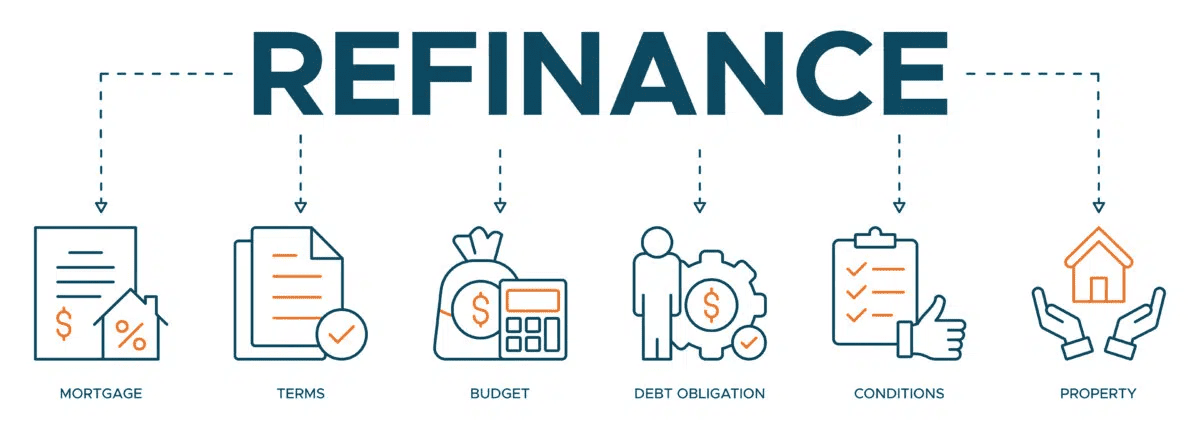

How to Refinance: The Step-by-Step Process

- Determine If a Refinance Makes Financial Sense: Calculate the break-even point.

- Shop and Compare Rates: Work with a broker to access rates from multiple lenders.

- Submit Your Mortgage Application: The process mirrors your original application — employment verification, income confirmation, credit check, and stress test. Insured mortgages must re-qualify at the higher of the contract rate + 2% or 5.25%.

- Home Appraisal: The lender orders an independent appraisal to confirm current market value and establish the maximum borrowing amount (80% of appraised value).

- Legal & Title Work: A lawyer or notary handles discharge of the old mortgage, registration of the new one, and title insurance. For a straightforward switch, this typically takes 1–2 weeks from approval.

- Fund the New Mortgage: On the closing date, the new lender pays off the old mortgage and any applicable penalties. Cash-out proceeds are deposited to your account.

The May 2026 Opportunity: What Brokers Should Be Saying

Key Talking Points: May 2026

1. The pause is a planning window. With the Bank of Canada on hold, rate stability gives clients time to analyze options without urgency pressure.

2. Many 2021 buyers are approaching renewal. Clients who took 5-year terms in 2021 will be renewing through 2026. A refinance at renewal is penalty-free and strategically smart right now.

3. Variable mortgage holders have a low-cost exit. With penalties of only 3 months’ interest, variable clients can switch to fixed inexpensively if they want payment certainty. 4. Equity has grown. Canadian property values have appreciated significantly in most markets. Many clients have far more borrowing capacity than they realize.

Does Refinancing Hurt Your Credit Score?

Yes—marginally and temporarily. Refinancing requires a hard credit inquiry, which reduces a credit score by a small amount in the short term. Once the new mortgage is in place and payments are made consistently, the score recovers and typically improves. This should not be a barrier for most clients with a solid payment history.

Final thoughts

Refinancing is not a one-size-fits-all strategy. It requires honest math, an understanding of each client’s timeline, and a clear view of what they’re trying to achieve. The brokers who add the most value in this market are the ones who run the break-even numbers, present the alternatives, and help clients make a genuinely informed decision.

In May 2026, with rates stabilized and a large cohort of Canadian homeowners approaching renewal, the refinance conversation has rarely been more relevant. The clients who stand to benefit most are those in higher-rate fixed mortgages approaching renewal, homeowners with significant equity who have not yet explored their options, and variable mortgage holders seeking payment predictability.

Help them run the numbers. Help them understand the costs. And when it makes sense—make it happen.

Ready to Start the Refinance Conversation?

Whether your clients are approaching renewal or exploring equity options, now is the time to run the numbers. The savings may surprise them.

Book a Strategy Call | Use Refinance Calculator | Contact Your Broker Today